The Canadian Mortgage Landscape: Fixed Rates On the Move

Hey there, fellow Canadians! Let's gather around the digital campfire and discuss something as thrilling as a double-overtime playoff game: mortgages. And not just any mortgages - we're talking fixed-rate mortgages.

The Lowdown on Fixed Rates

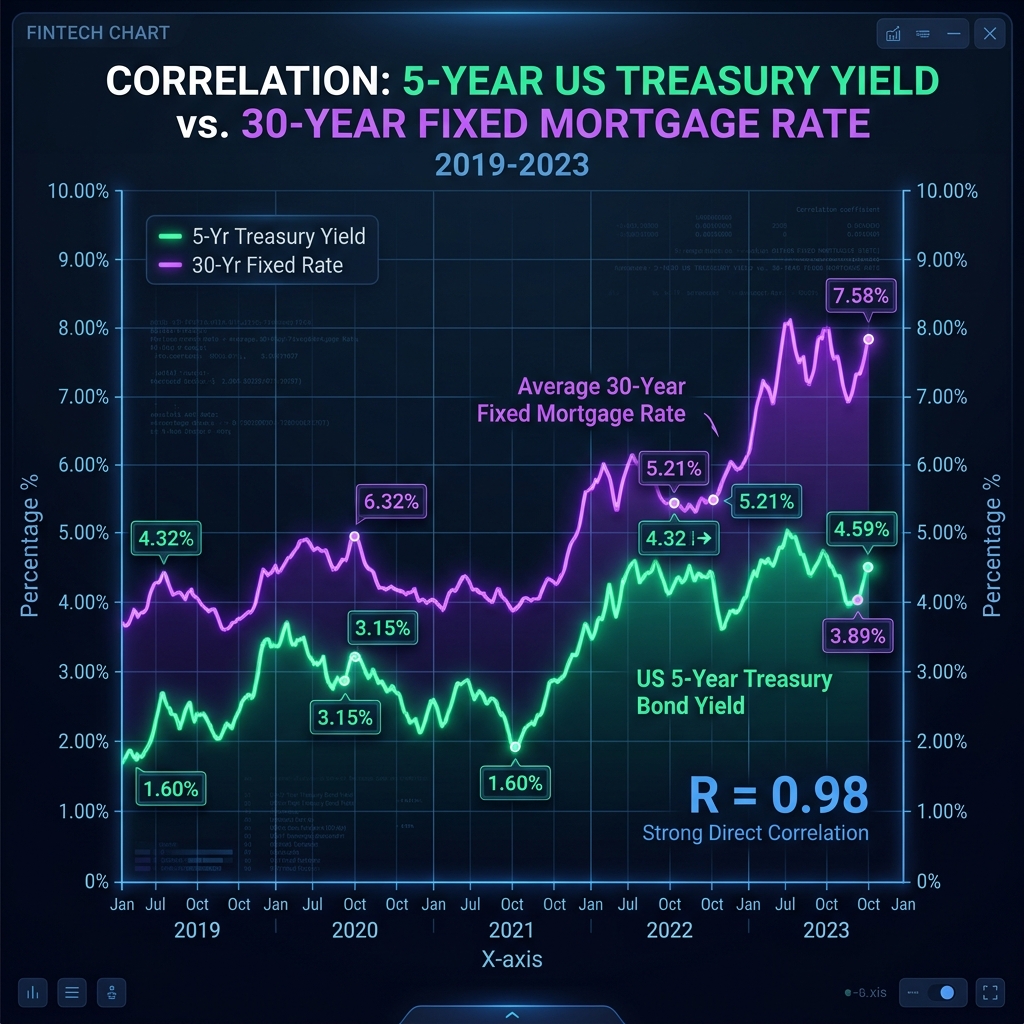

Remember when your biggest worry was whether your favourite hockey team would make the playoffs? Well, this might give you a similar feeling of suspense. The yields on Canada's five-year bond are performing a high-wire act.

So, you know when you're at a backyard BBQ and your friend, without fail, follows you to the grill? You've got this bond, right? Well, that's precisely what's going on between bond yields and fixed mortgage rates.

Let's break it down: Bond yields are like making a beeline for the grill. And the mortgage rates? That's your friend, sticking to you like a bee to honey. You pick up a burger, they pick up a burger. You grab a hot dog, and guess what? They're reaching for the mustard and buns.

So, next time you see bond yields making moves, don't be surprised if mortgage rates are right there with them, ready to snag a burger of their own. It's a bond as strong as my love for BBQ! Now, who's ready for seconds?

Oh, you want seconds? You got it! These yields aren't just going for a walk; they're sprinting north. Picture this: a day range soaring from 4.255% to 4.390%.

Now, here's where it gets interesting. There's typically an average cozy little gap of about 1.56% between the bond and the five-year insured mortgage rates. Think of it as the distance between your couch and the TV remote on a lazy Sunday.

So what do we do with this 1.56%? We add it to our bond rate, just like you'd add an extra spoonful of sugar to your coffee. And voila! You're now in the ballpark of where those fixed rates will likely land.

Bond Yield-Mortgage Rate: The Dynamic Duo

Let's play a game of connect-the-dots. Dot one: banks fund their fixed-rate mortgages by investing in government bonds. Dot two: when the return on these bonds (aka yield) goes up, the cost of borrowing for banks follows suit. Dot three: higher costs for banks mean higher mortgage rates for us. See the connection? It's like a financial domino effect.

Homeowners and Buyers: Take Note!

So, what does this mean for homeowners and potential buyers? If you're already snug as a bug with a fixed-rate mortgage, you can relax. Your interest rate and monthly payments are as secure as a goalie with a shutout going into the third period.

But if you're staring down at a mortgage renewal or thinking about getting a new mortgage, it's time to lace up your skates. These rising yields will lead to higher rates.

And for those eyeing a new home, this might make you reconsider your game plan. But here's the plot twist - these rate hikes could result in a decrease in house prices.

Let's Talk Numbers: House Prices and Interest Rates

You're probably wondering, 'Just how much could house prices drop?' I don't have a magic eight ball, but some experts predict that for every 1% increase in

interest rates, house prices could take a 5% hit.

Keep in mind, though, that the housing market is as unpredictable as a playoff series. It's influenced by all sorts of factors, from the economy to immigration rates. So, while interest rates are a major player, they're not the only ones on the ice.

The Final Whistle: What's Next?

Navigating the world of mortgages can feel like trying to understand the offside rule in soccer. But remember, knowledge is power. Staying informed about these changes can help you make the best decisions for your home financing options.

Feeling lost? Don't hesitate to reach out to us. We're like your personal coach, ready to guide you through the complex plays of the mortgage game.

So keep your head up and stick on the ice. It's going to be an interesting game.

Back to Main Blog Page