How to Qualify for a Mortgage in London, Ontario in 2026

Unlocking Your Borrowing Leverage in the London Ontario Housing Market

Buying a home in London Ontario under the 2026 lending guidelines requires a clear understanding of qualifying parameters. With London's benchmark housing price hovering around the $600,000 to $650,000 mark in early 2026, buyers who prepare their files early are securing the most competitive wholesale rates. Whether you are working with a mortgage broker London Ontario for your first purchase or moving up the property ladder, this guide maps out the exact underwriting criteria used by major institutional and alternative lenders.

The Core Qualifying Criteria: Credit, Income, and Debt Ratios

Lenders evaluate your mortgage application based on three key pillars. Understanding these thresholds determines your borrowing capacity and the rates you qualify for:

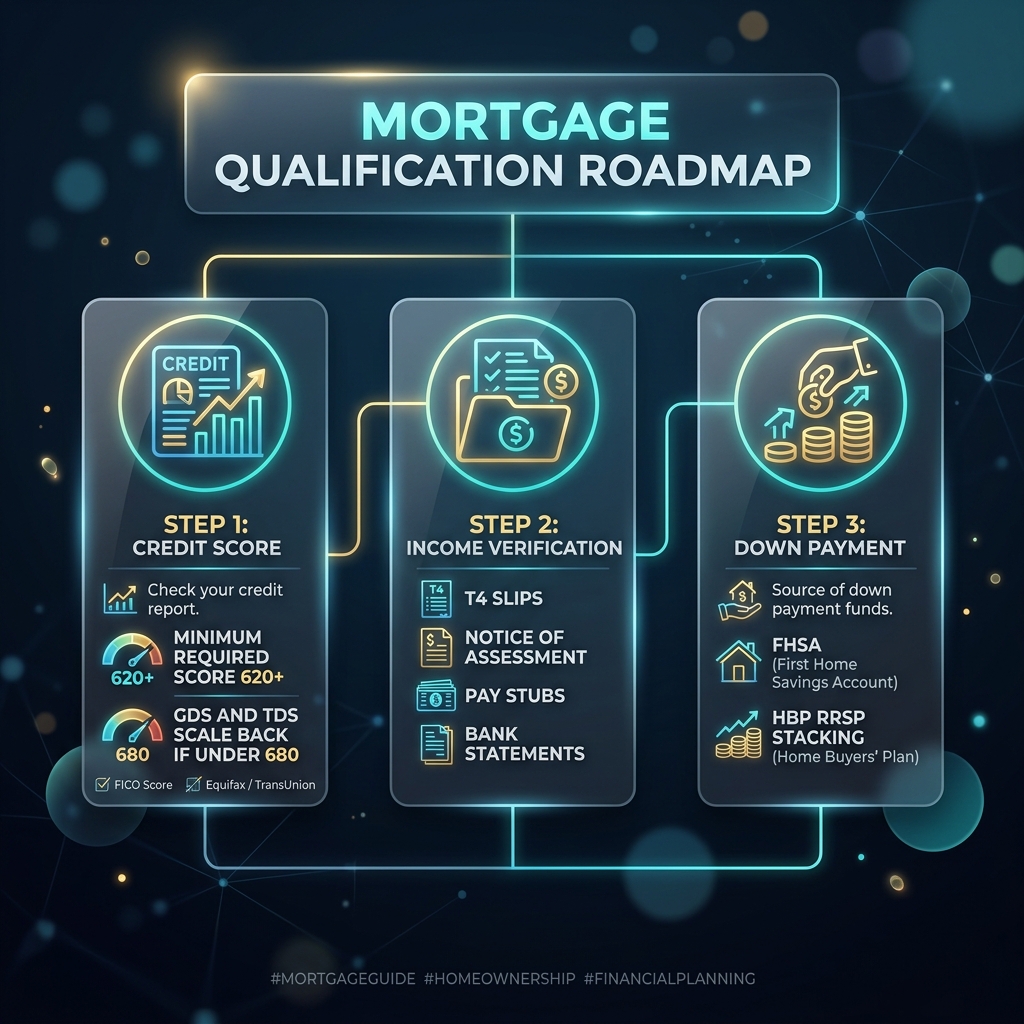

- Credit Score Thresholds: A credit score of 620 or higher is generally required to secure an insured high-ratio mortgage. If your credit score is between 620 and 679, you can still qualify, but underwriters will scale back your GDS and TDS caps (restricting your maximum borrowing capacity). For prime wholesale rates and maximum debt service ratios, a score of 680 or higher is required. Credit scores below 620 generally require conventional financing with a minimum 20% down payment.

- Debt Service Ratio Calculations: Underwriters analyze two primary ratios:

- Gross Debt Service (GDS): The percentage of your pre-tax income needed to cover housing costs (mortgage principal, interest, property taxes, and heating). This is capped at 39% for prime borrowers (and reduced to 35% for scores under 680).

- Total Debt Service (TDS): The percentage of your income needed to cover housing costs plus all other outstanding debt payments (credit cards, car loans, student loans). This is capped at 44% (and reduced to 42% for scores under 680).

2026 Home Purchase Qualifier (London Ontario)

Calculate your maximum buying power using official GDS/TDS debt service thresholds (39% / 44%) and the 2026 mortgage stress test.

Qualifying Estimate

Income Documentation: Preparing Your File

Documenting your income correctly is the most critical step in avoiding closing day delays. Lenders require specific paperwork depending on your employment structure:

For Salaried and Hourly Employees (T4)

If you are a traditional employee, you must provide:

- A recent letter of employment signed by your employer confirming your role, salary or hourly rate, and guaranteed hours.

- Your two most recent pay stubs showing year-to-date earnings.

- Your T4 slips and corresponding Canada Revenue Agency (CRA) Notice of Assessments (NOA) for the last two calendar years to verify income stability.

For Self-Employed Buyers

If you run a business or operate as an independent contractor, qualifying requires a deeper analysis. You will typically need to provide:

- Your T1 General tax returns and Notice of Assessments for the last two consecutive years.

- Articles of Incorporation or your Business Registration certificate to prove ownership history of at least two years.

- Two years of corporate financial statements if your business is incorporated.

If you do not show sufficient net income on your tax returns due to write-offs, you can access specialized self-employed mortgage programs that utilize business bank statement audits to prove cashflow.

Understanding Down Payment Rules and Stacking Options

In Canada, the minimum down payment is determined by the purchase price of the home. Here is how the tiers are structured:

| Purchase Price Band | Minimum Down Payment Formula | Example Down Payment ($1.2M Purchase) |

|---|---|---|

| First $500,000 | 5% of the purchase price ($25,000) | $25,000 |

| Portion from $500,001 to $1,499,999 | 10% of this portion | $70,000 (10% of remaining $700,000) |

| Total Minimum Down Payment | Tiered Calculation | $95,000 (7.91% average) |

For properties priced at $1,500,000 or more, a flat 20% minimum down payment is mandatory. For homes under this threshold, buyers can still access tiered, high-ratio insured structures. First-time buyers in London can stack their Tax-Free First Home Savings Account (FHSA) and Registered Retirement Savings Plan (RRSP) Home Buyers’ Plan (HBP) to build their down payment. For more details on stacking structures, visit our comprehensive first time buyers down payment strategy guide.

The 2026 Mortgage Stress Test Explained

Every borrower in Ontario must qualify under the federal stress test rules, even if they choose a fixed or variable rate with a lower contract rate. This policy is designed to ensure you can still afford your payments if interest rates rise in the future.

Under current rules, you must qualify at the higher of:

- Your contract interest rate plus 2%.

- The benchmark rate of 5.25%.

For example, if you secure a 5-year fixed wholesale rate of 3.99%, your debt ratios will be calculated using a qualifying rate of 5.99%. This stress test reduces your total buying power by approximately 15% to 20% compared to using the contract rate alone. Working with an independent broker allows you to shop multiple credit unions and alternative lenders, some of which are not federally regulated and can offer more flexible qualifying rates.

Uninsured Stress Test Renewal Exemption: If you already hold an uninsured mortgage and are looking to switch lenders at renewal, current regulations allow you to transfer your straight-in mortgage without being subject to the stress test. This is an essential exemption for homeowners looking to escape high renewal rates by shopping for the best wholesale rates across multiple lenders.

Expert Guidance from a Licensed Professional

Securing a mortgage is more than just finding the lowest rate online. It requires matching your personal financial profile with the underwriting guidelines of Canada's top institutional lenders. Dallas Martin is a licensed Mortgage Agent Level 2 (FSRA License #M17001133) operating under The Mortgage Firm (FSRA Brokerage Licence #13466). With access to over 50 lenders, Dallas specializes in structuring custom mortgages for first time buyers, self-employed individuals, and families looking to refinance or access home equity. Contact Dallas Martin today to start your pre-qualification audit.

Our Trusted Lenders

Through our partnership with The Mortgage Firm, we negotiate directly with Canada's top institutional and private equity lenders.