Advanced Co-Signing and Guarantor Mortgage Structures: Saving LTT and Capital Gains

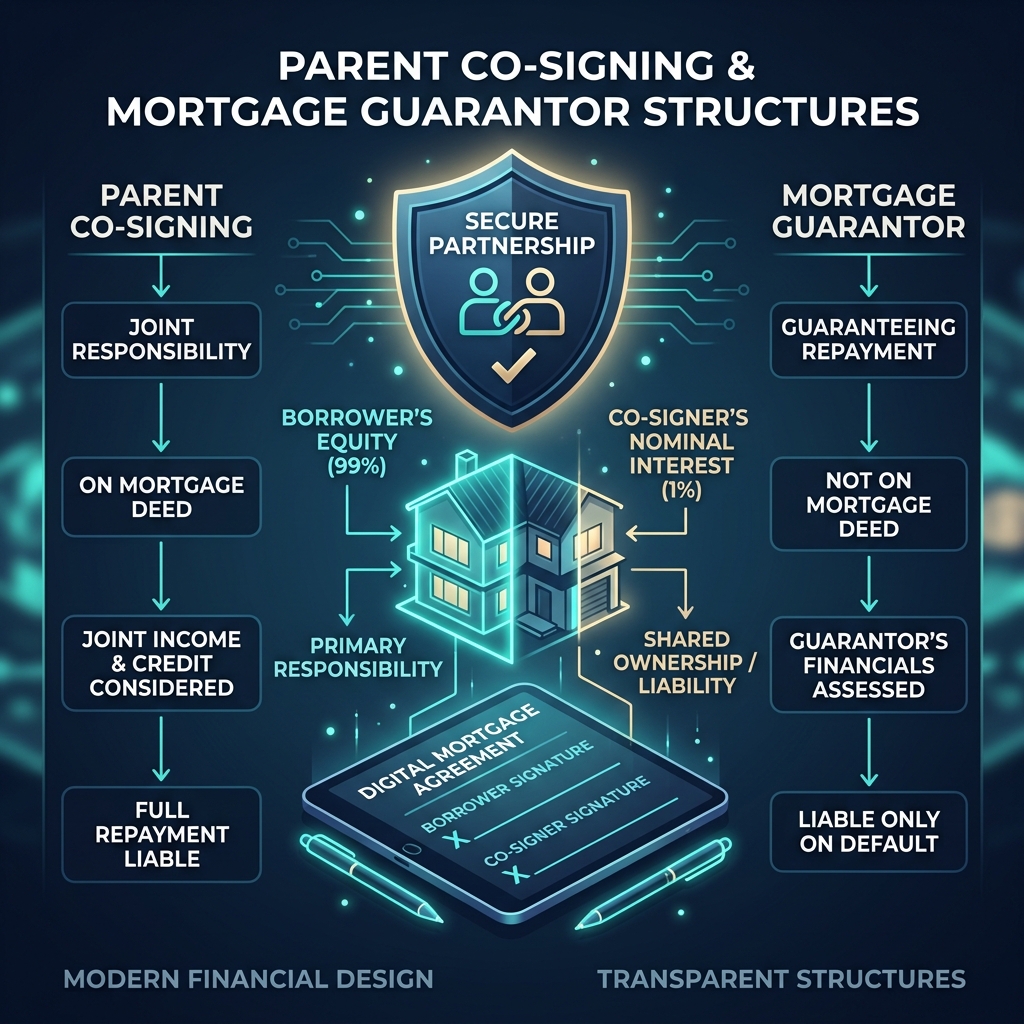

The Risks of standard Parent Co-signing Agreements

With strict debt service ratios and rising home values, many first time buyers require a parent or family member to co-sign on their mortgage application to qualify. While co-signing is a common underwriting solution, adding a parent to the home title without a strategic legal structure triggers massive, hidden tax liabilities.

If a parent is simply added to the title as a 50% joint owner, they face two severe financial penalties under Ontario legislation:

- Forfeiture of Land Transfer Tax Refunds: First time buyers qualify for a Land Transfer Tax (LTT) refund up to $4,000. If a parent (who is not a first time buyer) owns 50% of the home, the LTT refund is instantly cut in half, costing the family $2,000 in cash on closing day.

- Capital Gains Exposure: Because the home is not the parent's principal residence, the parent's 50% share of the property is subject to future capital gains tax when the property is eventually sold or transferred, yielding thousands of dollars in unnecessary tax liabilities.

The Underwriting Solution: The 99-to-1 Tenants-in-Common Title Split

To satisfy bank underwriters while completely protecting the family's tax advantages, real estate lawyers utilize a structured ownership split known as Tenants-in-Common with a 99% to 1% Title Split.

Instead of registering the property as a standard 50/50 Joint Tenancy, the title is structured so that the first time buyer child owns 99% of the property, and the co-signing parent owns only 1%. Here is how this mathematical split works on a typical $600,000 purchase in London, Ontario:

| Tax and Liability Metric | Standard 50/50 Title Split | 99/1 Tenants-in-Common Split | Direct Family Savings |

|---|---|---|---|

| LTT First Time Buyer Refund | $2,000 (Reduced by 50%) | $3,960 (99% Intact) | +$1,960 Cash on Closing |

| Parent's Capital Gains Exposure | 50% of home appreciation | Restricted to just 1% | 98% Capital Gains Reduction |

| Underwriter Compliance | 100% Approved | 100% Approved | Both models satisfy bank qualifications. |

The Alternative: Off-Title Mortgage Guarantor Status

If a parent has exceptionally strong credit and income, we can negotiate with specific institutional lenders to have the parent sign as an off-title Mortgage Guarantor. Under this structure:

- The parent's strong income fully backs the mortgage to secure approval.

- The parent is registered 0% on the property title.

- The first time buyer child retains 100% ownership, securing the full $4,000 LTT refund and completely eliminating the parent's capital gains exposure.

Not all banks allow off-title guarantors, which is why working with an independent mortgage broker is critical to accessing lenders who accommodate this structure.

Navigating Underwriting and Title Split Guidelines

Structuring a co-signed mortgage correctly requires seamless coordination between your mortgage broker and your real estate lawyer. Speak with Dallas Martin today to run exact debt-to-income calculations and map out a co-signing structure that protects your family from unnecessary taxation.

Our Trusted Lenders

Through our partnership with The Mortgage Firm, we negotiate directly with Canada's top institutional and private equity lenders.